Case study: How to handle form 8962 when divorced parents share a marketplace plan

Introduction

Navigating the complexities of IRS Form 8962 can be challenging, especially when multiple tax families share a single Marketplace health insurance policy. A common scenario involves divorced parents who each claim one child as a dependent but are covered under the same policy. This raises critical questions about filing obligations, allocation strategies, and potential IRS scrutiny.

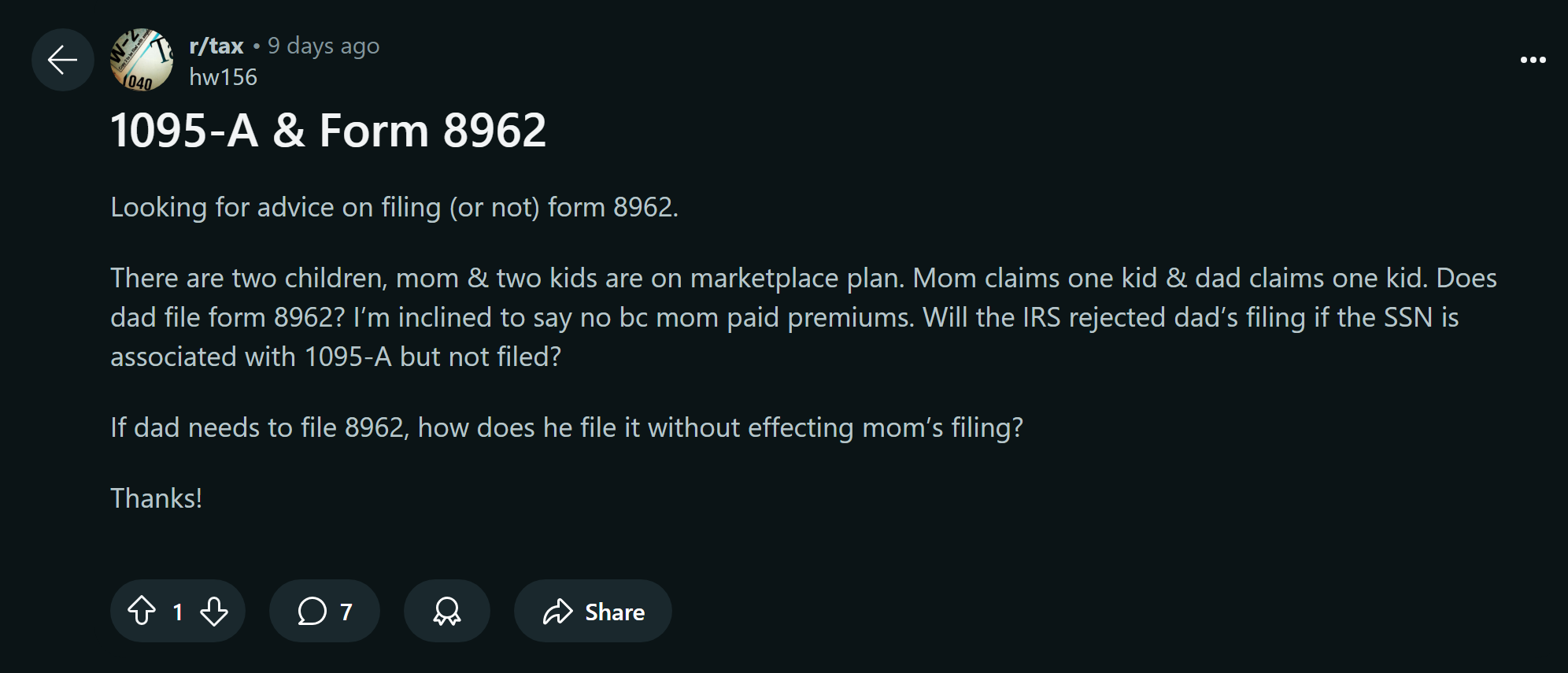

In this case study, we’ll address a specific question from a taxpayer seeking clarity on whether the non-premium-paying parent (the father) must file Form 8962 (download the form here), how to avoid IRS rejection, and how to coordinate filings between both parents. Drawing on IRS guidelines, tax software documentation, and expert insights, we’ll provide a step-by-step breakdown of the requirements and best practices.

The Question

Question about 1095-A & Form 8962 on Reddit

The Answer

The reconciliation of premium tax credits through IRS Form 8962 remains a critical yet complex component of tax compliance for households with Marketplace health insurance. This report examines the filing obligations for parents sharing a policy under divergent tax-family structures, focusing on scenarios where one parent claims one child while the other parent claims another. Drawing on IRS guidelines, tax software documentation, and practitioner insights, this analysis clarifies the conditions requiring Form 8962 completion and the procedural safeguards against IRS rejection.

The Affordable Care Act mandates that taxpayers reconcile advance premium tax credits (APTC) with their final eligibility based on household income, as outlined in the IRS instructions for Form 8962 and Healthcare.gov’s tax form overview. Form 8962 serves as the mechanism for this reconciliation, requiring proportional allocation of policy amounts when multiple tax families share coverage. Failure to file the form when required triggers IRS scrutiny, as the agency cross-references 1095-A data with tax returns.

Definition of “Tax Family” and Allocation Rules

A “tax family” comprises individuals claimed as dependents or included in a taxpayer’s household for premium tax credit purposes, as defined in the IRS instructions for Form 8962. When a Marketplace policy covers individuals from separate tax families (e.g., divorced parents each claiming one child), Allocation Situation 4 under IRS guidelines applies, as detailed in TaxSlayer Pro’s shared policy allocation guide:

Mandatory Participation: All policyholders must file Form 8962 regardless of premium payment responsibility.

Flexible Allocation Percentages: Parties may agree to any allocation split (e.g., 100%-0%, 75%-25%) provided the total equals 100%, as discussed in Intuit Community discussions.

Dispute Resolution Default: If parties cannot agree, allocations default to percentages proportional to covered individuals in each tax family.

Application to Parental Claims Scenarios

Case Study: Divorced Parents with Dual Dependents

Consider a divorced mother and father where:

Mother claims Child A as a dependent

Father claims Child B as a dependent

All four individuals (mother, father, two children) share a single Marketplace policy

Mother paid 100% of premiums

Mother’s Obligations

Form 8962 Requirement: The mother must file Form 8962 because she received Form 1095-A and claimed APTC, as per the IRS instructions for Form 8962.

Allocation Strategy:

Part IV Allocation: Designate 100% responsibility to herself, citing the father’s SSN as the shared taxpayer, as explained in TaxSlayer Pro’s allocation examples.

Monthly Calculations: Apply 100% of SLCSP premiums and enrollment amounts to her reconciliation.

Father’s Obligations

Form 8962 Requirement: Despite not paying premiums, the father must file Form 8962 because:

Form 1095-A Reporting: Attach a copy of the mother’s 1095-A to justify $0 reconciliation, as recommended in Intuit Community discussions.

Key Precedent: In Intuit Community Discussion 3260136, TurboTax experts confirmed that 0% allocations remain valid if both parties report complementary percentages.

Procedural Safeguards Against IRS Rejection

Documenting Shared Policies

Cross-Referencing SSNs: Both returns must list each other’s SSNs in Part IV to establish an audit trail, as outlined in TaxSlayer Pro’s allocation examples.

Form 1095-A Distribution: The policyholder (mother) must provide copies to all allocated parties (father) to ensure consistent reporting, as emphasized in FreeTaxUSA’s guidance.

Forced Allocation Matching: TurboTax and TaxSlayer Pro require shared policy SSNs and percentages to prevent mismatches, as discussed in Intuit Community discussions.

Error Suppression: Entering 0% allocation with proper SSN documentation avoids “unreconciled APTC” flags, as noted in Reddit tax discussions.

Risks of Non-Compliance

Audit Triggers

SSN Mismatches: Unreported 1095-A entries for Child B’s SSN on the father’s return generate IRS Notice CP087, as highlighted in Healthcare.gov’s tax form overview.

Premium Tax Credit Discrepancies: Failure to reconcile APTC across both returns risks recapture of credits plus penalties, as outlined in the IRS instructions for Form 8962.

Mitigation Strategies

Proactive Disclosure: File Form 8962 with 0% allocation even if no APTC was received, as recommended in Intuit Community discussions.

Alternative Calculations: For divorced parents, IRS Publication 974 permits retrospective adjustments if marital status changes mid-year, as detailed in the IRS instructions for Form 8962.

Conclusion

The father must file Form 8962 despite not paying premiums. Key steps include:

Mother’s Return: 100% allocation with father’s SSN in Part IV.

Father’s Return: 0% allocation with mother’s SSN and attached 1095-A.

This dual filing satisfies IRS matching protocols while insulating both parties from penalties. Practitioners should emphasize that premium payment responsibility does not override the shared policy reporting mandate under §36B of the Internal Revenue Code, as outlined in the IRS instructions for Form 8962. Future disputes may be mitigated through pre-filing allocation agreements documented via Form 8857.